Are Income Lab guardrails based on Guyton-Klinger guardrails?

Income Lab guardrails are not the same as Guyton-Klinger guardrails. Income Lab guardrails are "risk-based" and much more powerful and accurate than static withdrawal-rate-only guardrails.

Last published on: November 14, 2025

Income Lab Risk-Based Guardrail are not Guyton-Klinger Guardrails (and that's a good thing!)

The first type of “guardrails” for retirement income that many people encounter are Withdrawal Rate Guardrails, such as those proposed by Jonathan Guyton and William Klinger in a series of articles in the early 2000s (the so-called “Guyton-Klinger Guardrails”). There are some good aspects to Guyton-Klinger guardrails. However, research shows that there are much better guardrail approaches available.

It is important to understand that the guardrails you see in Income Lab are not Guyton-Klinger Guardrails. Instead, Income Lab guardrails are holistic “risk-based guardrails”. Risk-based guardrails incorporate all that is good about withdrawal rate and Guyton-Klinger guardrails, but are more holistic and provide better performance in the real world. If you've been using Guyton-Klinger guardrails, no problem! You've come to the right place. There are many good reasons to move to Risk-Based Guardrails and the transition is easy.

While Guyton-Klinger guardrails have the advantage of being fairly well known and easy to calculate, they have the disadvantages of performing very poorly in practice (they often result in large - and ultimately unnecessary - reductions in spending over time) and not being applicable to many very common planning situations.

Problems with Guyton-Klinger Guardrails:

- Cannot handle real-world planning situations where expected non-portfolio income and/or spending needs change over time

- Perform very poorly when run through historical returns and even hypothetical scenarios

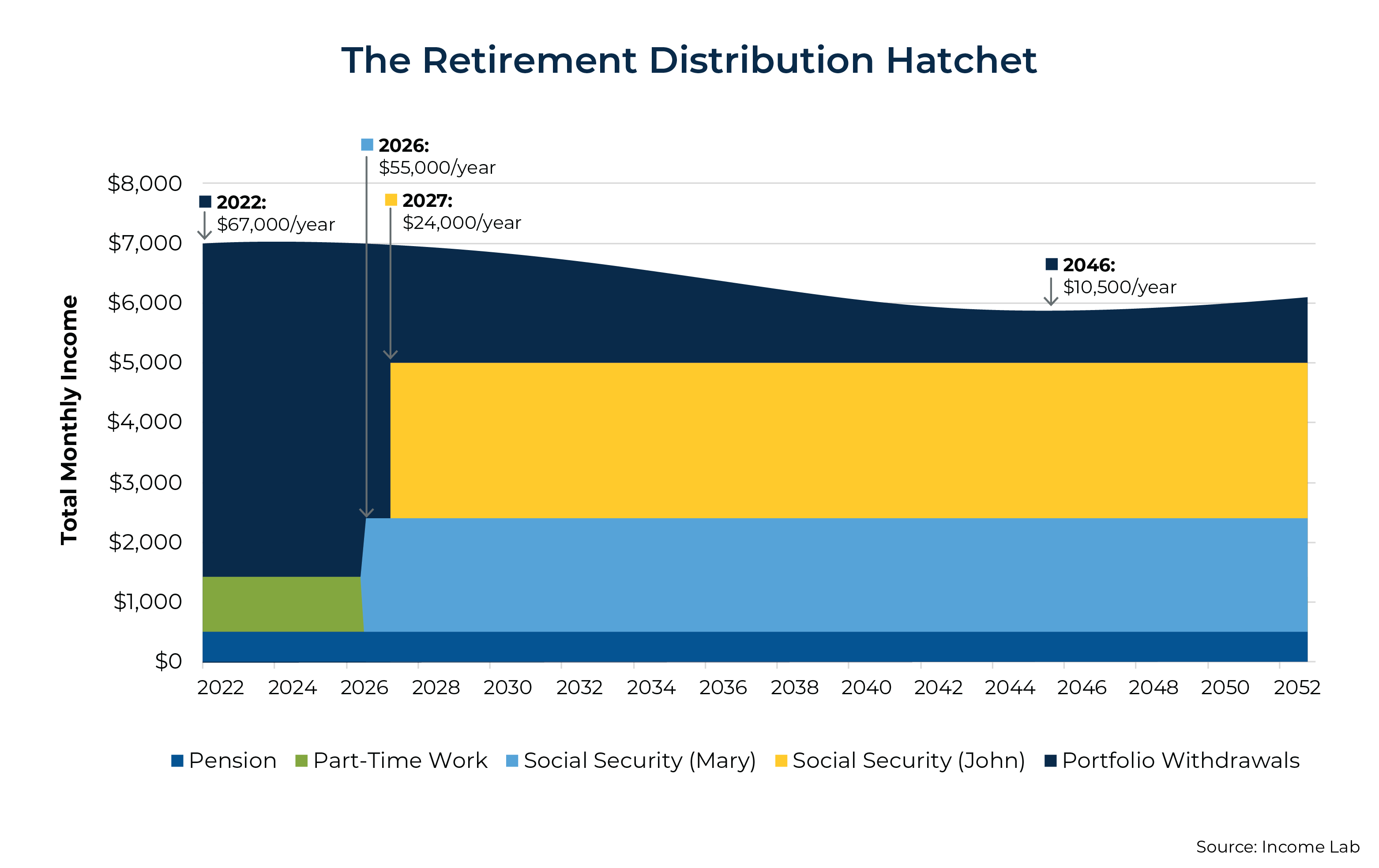

Taking the first problem first, because Guyton-Klinger guardrails are based on withdrawal rates, they cannot handle real-world plans where non-portfolio income is not expected to be steady over time or where income needs are not expected to stay constant at all ages. In either of these situations, planned withdrawal rates would be changing, either because total spending needs have changed or because a non-portfolio income stream has come or gone, meaning a planned change in needed portfolio withdrawals. This situation is sometimes called the “Retirement Distribution Hatchet” because the shaped of the projected need for withdrawals is shaped like the blade of a hatchet, followed by the handle (once other income sources like Social Security begin).

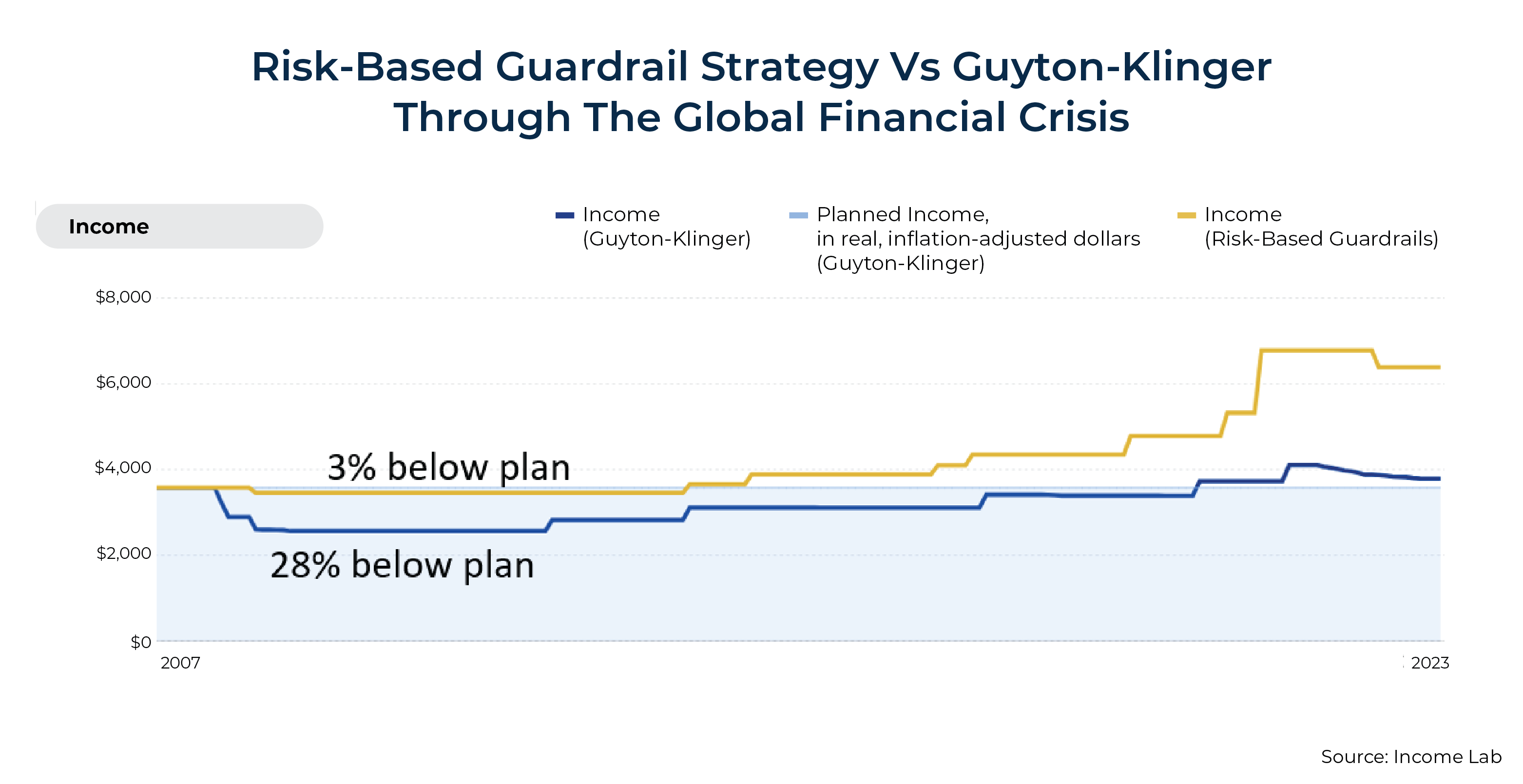

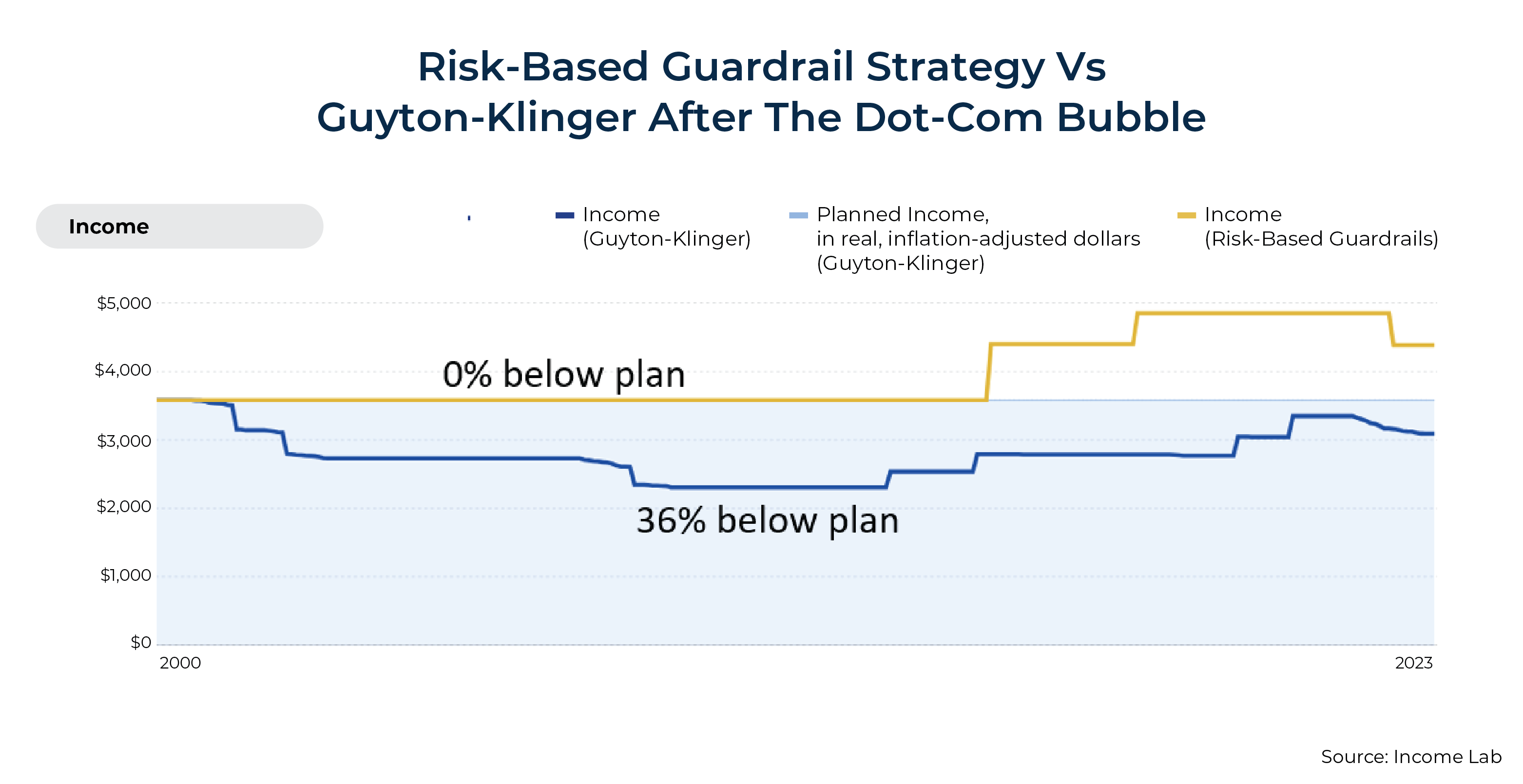

Furthermore, even for plans where income and non-portfolio income are steady, research shows that Guyton-Klinger Guardrails perform very poorly in real life. This poor performance comes from at least two sources.

- Any guardrails that are defined only by withdrawal rates will fail to account for other risks in retirement, like mortality risk and inflation risk.

- Fixed percentages do not reflect the fact that as time goes on the plan changes. For example, what is a safe withdrawal rate for a 60 year old is a very low withdrawal rate for a 75 year old. Research shows that using static withdrawals rates to guide changes in spending leads to deep cuts in spending that are not needed.

Comparing Guyton-Klinger and Risk-Based guardrails in real historical scenarios shows how Guyton-Klinger guardrails result in deep cuts to spending in tough times.

One reason risk-based guardrails perform better is that they change over time. The explicit guardrails in any guardrail system should change over time. Why? Because the facts on the ground are changing: the ages of the clients, the returns and inflation that have been experienced, and so on. If you have the same guardrails at 75 that you had at 60, something's wrong!

For an in-depth look at these problems, and discussion of the difference between risk-based and withdrawal-rate guardrails, please see the following articles.

- Why Guyton-Klinger Guardrails Are Too Risky For Most Retirees (And How Risk-Based Guardrails Can Help) - Kitces.com

- The Retirement Distribution “Hatchet”: Using Risk-Based Guardrails To Project Sustainable Cash Flows - Kitces.com

- The Guyton-Klinger Archives - EarlyRetirementNow (Karsten Jeske)

- Making Sense Out of Variable Spending Strategies for Retirees - Journal of Financial Planning (Wade Pfau)

(The underperformance of Guyton-Klinger guardrails shown above was also found by Pfau and Jeske in both historical and Monte Carlo testing.)

Making the Transition to Risk-Based Guardrails

Luckily, if you've been using withdrawal rate guardrails like Guyton-Klinger guardrails, the shift to risk-based guardrails is very easy. First, the conceptual framework (the way that clients think about the method) is exactly the same for both approaches:

- Upper guardrail: We're not spending as much as we could. Our risk of underspending and regret is high. It's time to live a little.

- Lower guardrail: We're running too hot. Our risk of overspending is too high. We're spending too much or have too big of future spending goals given our resources. It's time to tap the brakes.

(For more on the overspending/underspending framework, see Reframing Risk In Retirement As “Over- And Under-Spending” To Better Communicate Decisions To Clients, And Finding “Best Guess” Spending Level on Kitces.com.)

Furthermore, Risk-Based Guardrails not only allow you to state the guardrails in dollar terms (a portfolio balance where a change would be prudent), but even the projected change in spending is explicit. You'll see both of these on the Income Dashboard.

We have heard from advisors who used to use Guyton-Klinger guardrails and switched to Income Lab that they experienced zero client push-back during this transition. If needed, the explanation for this shift goes something like this:

💡Explaining the transition to clients

“We're always looking for new techniques and technologies to help us better serve you. We're shifting from a very simple ‘withdrawal rate’ approach to a much more holistic and powerful guardrail system that covers not just investment risk but other important risks, like mortality and inflation, and better adapts to changes over time. You can view this as a natural evolution of the approach we already had. This will help us provide better advice to you as we walk with you through retirement."